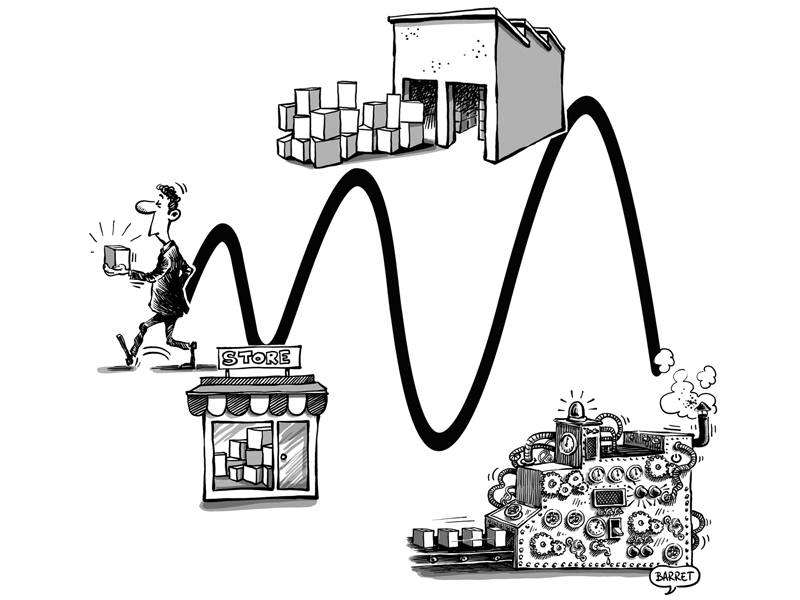

The bullwhip effect

The rise in final demand has sent shock waves through production lines. Should we fear a lasting return of inflation?

Pandemic-related confinement and forced savings – brought about in part by the tremendous fiscal momentum in both the United States and Europe – have supported, and in some cases even increased final demand for manufactured goods. This recovery at the end of the value chain was amplified by each link in the production chain, anxious to respond to their customers and have sufficient stocks, to the point of causing a shock wave and increasingly glaring supply disruptions. The spectacular rebound in world trade since the summer, after the apathy of last spring, the increase in demand for semiconductors as the auto industry begins its conversion, the surge in commodity prices, have produced this “bullwhip” effect, which causes the recent rise in producer prices and threatens to spread to the final CPI. And since a problem never happens on its own, here in Taiwan, the drought threatens to further delay the deliveries of the precious silicone elements. At other points in the chain, it is the ports that lack manpower to unload the boats, or the containers that remain blocked where they are delivered to serve as additional storage capacities, instead being returned to merchant ports. For a few months now, the big logistics companies have been on alert. or even containers that remain blocked where they are delivered to serve as additional storage capacities, instead of returning to merchant ports. For a few months now, the big logistics companies have been on alert.

Thus, the Covid-19 crisis has reserved its share of surprises. While the world was experiencing the worst recession in its post-war history, household incomes were generally preserved and even, in some cases, increased thanks to the budgetary measures deployed by the States. In the United States, the average household income would have increased by nearly 7% in 2020, despite the crisis. Likewise, in the United Kingdom, Germany and France, households have been particularly protected by budgetary support measures. In other countries, companies have seen their cash flow grow, and are ready to invest.

At the other end of the value chain, the trade war already underway, the arbitrations of the oil-producing countries, the race for autonomy as well as the realization that the security of supplies now labeled strategic require greater control, only accentuate these tensions. Producer prices are rising and experts are gradually revising their consumer index forecasts. So far, the denials of the Federal Reserve and its sisters have done nothing, the yields of US and European debt have increased, causing concern on the stock markets.

Should we be alarmed? As activity restrictions are lift – and vaccination campaigns can only give us hope – the global economic recovery should indeed exceed its potential. This acceleration of the “output gap” should nevertheless prove to be temporary. The gradual decline in budgetary support measures, the accumulation of public debts, and unemployment stabilized above its pre-crisis levels, leave little room for the lasting persistence of these tensions. A few clues, still tenuous, seem to support this thesis: recently, the Chinese authorities were worried about a risk of overproduction of steel – and therefore of a fall in prices which would affect their industry.

The reorganization of production chains is still underway. This will take time. Will it be for the benefit of regions with higher average wages? In the United States, the administration intends to give priority to the relocation of semiconductor production. A gradual increase in the sector’s overall production capacities can only ease tensions. Other unknowns persist: it has been noted that unlike previous crises, the fall in investment has not been more marked than growth itself. Would this presage a rebound or a persistence of overcapacity and obsolescence? Will the stimulus packages emphasize the use of green energies and serve to increase the productivity of these sectors, or will they be the source of lasting upward pressure on prices?

Central banks in unison have reaffirmed their confidence in the gradual normalization of these trends. It should be remembered that we are still living under the yoke of significant restrictions, which are hampering the resumption of entire sectors of activity into which the flow of accumulated savings should flow. New regions of the world, such as India or certain African countries, could be the main beneficiaries of these reorganizations.

Getting interest rates out of the limbo into which they have fallen would be more favorable to this normalization. As with the conquest of space, “perseverance” is essential, even if the landing is not always well controlled.

Original text in French published in Allnews.ch March 3rd. ©Cartoon by Barret

{kind=link}