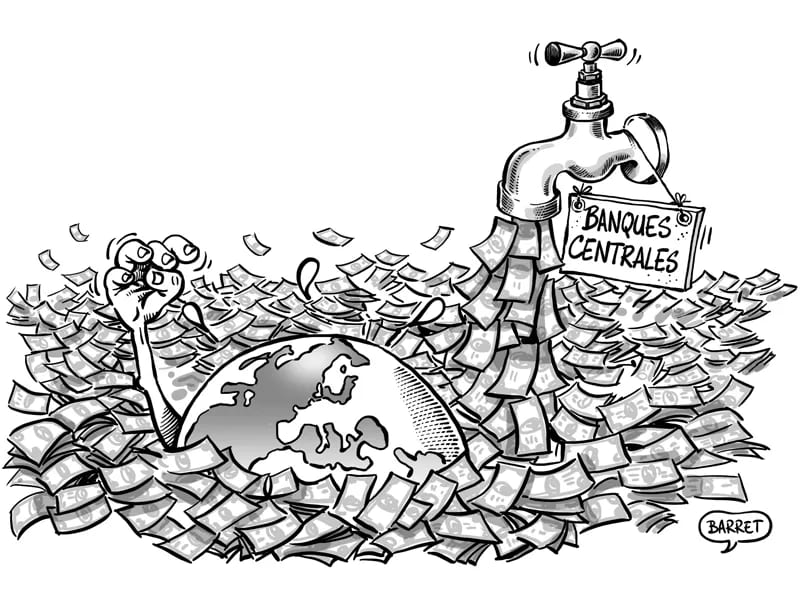

Flooded with cash

Central banks have become “lenders of first resort”. Shouldn’t they return this role to traditional banks?

Containment will surely have unexpected effects. It may be that the current crisis is helping to restore the image of teachers and professors to all parents who are now forced to go to school at home! The health personnel and all those who continue to work to provide the logistics essential to our lives, deserve our full recognition and support.

In terms of health, major maneuvers are launched. The United Kingdom and the United States now support the principle of containment. A comparative study by Imperial College London 1 , the Italian case after that of Wuhan, shows that it helps to reduce the saturation of hospital systems, that is to say ultimately the number of deaths .

The Bank of Japan has already gone so far as to buy stocks directly.

But as containment expands, will the economy have to be killed to kill the virus? Faced with this “Devil’s alternative”, states are launching increasingly massive safeguard plans, aimed at compensating for the losses of activity suffered by almost all sectors of the economy. In addition, the thirst for cash is such that it is all the “piping” of the financial system that threatens to implode. Tensions on the US repo market last fall had already given us a taste of the risks involved 2 . The widening of bond yields in the euro zone last week also sent us back to the painful memories of 2011-2012.

After the first failures, the central banks adjusted and stepped up to ensure the necessary liquidity for the system. The measures taken are of three types: They concern first of all massive purchases of public and private debts. An extension in volume but also in quality, since the Federal Reserve will buy municipal vouchers or commercial paper. The ECB will extend its debt purchases to Greece and increase those of Italian debt, beyond the current distribution rules. For its part, the Bank of Japan has already gone so far as to buy shares directly (the monetary authorities of Hong Kong had done so during the Asian crisis of 1997-1998). Then, the Federal Reserve concluded swap agreements in dollars with the main central banks in order, again, to counter the drying up of the markets and the panic in prices. Finally, the monetary authorities have decided to relax the prudential and accounting rules applied to the banking system in order to allow or even encourage the latter to increase its credit facilities.

Banks no longer play their role as natural funding vehicles.

It is on this last point that I would like to emphasize. The measures taken by the supervisory authorities during this crisis, which could therefore only be temporary, in fact reveal the shortcomings of regulatory reforms after the subprime crisis. These measures have left central banks alone on the front line in the face of an almost impeded system of financing the economy, by transferring to others, outside of any effective control, the financing of the economy. It is not a question here of calling into question a diversified and competitive organization of the financing of the economy and the markets, nor of abolishing any form of risk control. Care should be taken to ensure that lenders of first resort – those who actually create money – are able to manage time and ensure the spread of credit throughout the economy. By depriving the traditional banking system of its main transformative function, central banks have deprived themselves of their natural intermediaries and have lost the vectors of the transmission of their policy to the rest of the economy. The absence of inflation in final prices masked these shortcomings; it did not prevent the inflation of other price bubbles, the consequences of which nevertheless had to be remedied. Central banks have deprived themselves of their natural intermediaries and have lost the means of transmitting their policies to the rest of the economy. The absence of inflation in final prices masked these shortcomings; it did not prevent the inflation of other price bubbles, the consequences of which nevertheless had to be remedied.

The current crisis has such special characteristics that it cannot be compared to previous ones, particularly that of 2008, as to its origins. On the other hand, the chain of events it implements has led central banks a little further down the perilous path of direct financing of the economy. It is not their role. It is high time to put the traditional banking system back at the heart of the financing circuits of the economy.

First published in French for Allnews.ch

Image © Barret March 24 2020

{kind=link}